What is it they say about mixing your drinks? It certainly doesn’t end well if you combine the volume losses of the ale , lager , wine , spirits and RTD sectors in the past year. We’ve got through 63.9 million fewer litres of the stuff, a fall of roughly one litre per head [Nielsen 52 w/e 12 October].

But we’re not all on the wagon just yet, despite the best efforts of the health lobby (though lower-abv wine and beer ’s growth is gathering pace). cider , perry, sparkling wine and Champagne are in volume growth. Why? And can anything be learned from them?

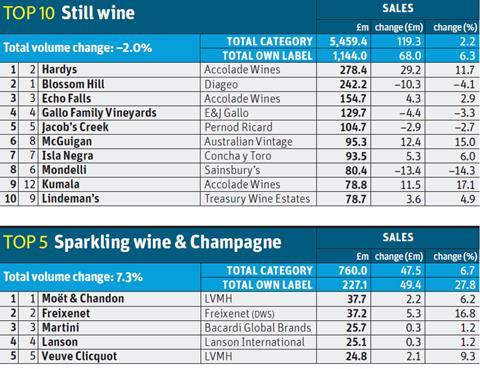

The sparkling wine and Champagne sector has been the standout winner of the past year, with value up 6.7% on volumes that have surged 7.3%. According to Chris Ellis, commercial director for wines at Pernod Ricard, much of this growth is down to a very simple desire: to show off. “Sparkling wine is currently outperforming the other wine categories,” says Ellis. “We see this trend continuing as consumers make purchases to impress family and friends at special in-home occasions such as dinner parties.”

So cheap plonk’s out. But we’re not going too posh. Despite the fact that we’ve popped roughly 140,000 more bottles of the top three Champagnes (Moët, Lanson and Veuve Cliquot) in 2013, it’s actually cheaper own-label and retailer exclusive brands - such as Sainsbury ’s Clevecy (up 15.3% in value 14.5% in volume) - that are driving the growth.

Apart from the poshest Champagnes, which despite high prices remain bulletproof (the top three sell for £37.73 a litre on average Clevecy fetches £15.60), brands are suffering, and that includes cavas, proseccos and other sparkling wines. Jacob’s Creek sparkling and Cordorniu cava have been hit by volume falls of more than 20% as they’ve fought own-label Champagne, and lost.

Only cava brand Freixenet, in second place, has held up against the onslaught, posting strong growth thanks to distribution gains, advertising and deals, which have driven down average price 1.7% to just £8.85 a litre.

Top products: Alcohol - The vital statistics

The rise of own label in sparkling makes it unique it’s the only drinks sector that has seen average prices fall, albeit by only 0.6%. In still wine, most accept that the sector’s 2.2% value growth has been driven by price increases, which have depressed volumes. “It would be naïve to deny that inflation and duty are affecting the price rises,” says Paul Schaafsma, Accolade Wines’ general manager. “However, we’ve engaged in a strategy to build value, as can be seen in the performance of Hardys and Kumala.”

The investment does indeed appear to be paying off, with most of Accolade’s major brands outperforming the market. Pernod Ricard’s Campo Viejo (up 25.9% on volumes up 26.8%) is also performing well. “Premiumisation is a key trend in off-trade wine, with premium brands like Campo Viejo outperforming other brands,” says Ellis.

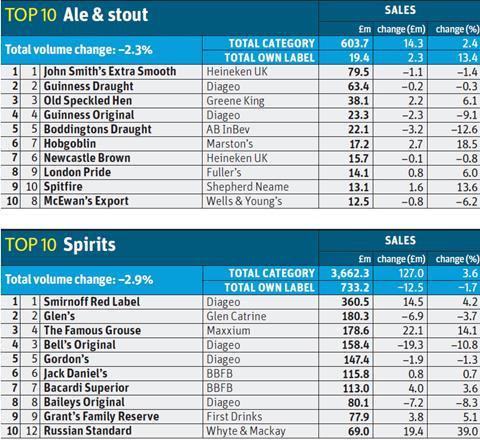

There’s further proof our tastes are getting more expensive in spirits. Gordon’s, for example, is falling fast, while pricier Tanqueray is up 15.6% on volumes up 8.8%. That’s despite the latter costing an average £6.08 more a litre. “We can see evidence that consumers are trading up from Gordon’s to Tanqueray,” says Diageo off-trade head Katherine Abram.

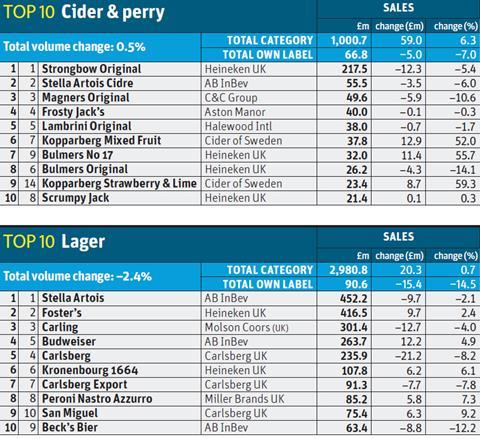

It seems we’re prepared to pay more for better quality in cider, too. Now a £1bn market for the first time in the off trade, cider’s prices have risen most steeply, by 5.7%, yet volumes have continued to rise (just). This is partly down to growth in fruit ciders, which generally carry a higher price tag as they pay a higher rate of tax than apple ciders.

But the growth isn’t all going to the taxman. Heineken UK’s trade & category marketing director Craig Clarkson says there’s plenty left of the respective 18% and 27% premiums new launches Strongbow Dark Fruit and Bulmers Bold Black Cherry carry over from the original versions once the Chancellor has taken his cut. “It’s important we add value to the category with NPD and everyone through the chain feels we are adding value,” he says.

Which is where mainstream lager has come unstuck. While we’re drinking more world and craft beers (no wonder Greene King opened a new craft brewery last month), we’re being asked to pay more for mainstream brands that have hardly changed in years. More of us are refusing.

The changes some brands have made have been particularly damaging, says one supermarket buyer: “Some have destroyed their brand equity by reducing abv under the guise of CSR. The real reason has been duty benefits. It would be helpful if brands with real authenticity were given some investment to inject excitement back into the category.”

Has the cross-industry Let There Be Beer campaign helped? “Not from my perspective,” says the buyer.

Top launch: Baileys Chocolat Luxe Diageo

Life hasn’t been too sweet and creamy for Baileys of late. Its value sales have fallen 8.3% and volumes are down an eye-watering 13.6%. But this new launch could really help pep things up for the brand. Developed by Anthony Wilson, whose father invented the original Baileys Irish whiskey , Chocolat Luxe contains Madagascan vanilla and 30g of Belgian chocolate per bottle. It taps the trend for more premium spirits and chocolate too, and has a £16.99/50cl rsp to match.

No comments yet